From 35,000 feet

2 weeks of strong markets made investors forget the Iran crisis. The level on the 10-yr is where the forgetting ends.

Weekly Snapshot

The Big Forgetting. Two weeks of strong performance, and AI has made investors forget the Iran crisis - just as it made them forget the tariff crisis a year ago.

The AI Distortion. Per the WSJ, the US AI economy grew 31% last quarter; the rest grew 0.1%. Mag-7 earnings up 61%, the other 493 up just 16%.

The Picks-and-Shovels Trade. Korea up 78% YTD. Taiwan now running a trade surplus equal to 24% of its GDP. Even bullish fund managers concede the hyperscalers themselves may not earn the capex back.

The ERP Question. Anthropic’s products are getting complex enough to look like enterprise software. Is that the new SAP - with a power-utility-sized capex base?

The Watch Level. Trump–Xi meeting on 14–15 May. Nvidia earnings 20 May. 10-year Treasury yields at 4.4% are the line. Watch the bond market.

For the past two weeks I have been looking at the world from somewhere between 30,000 and 38,000 feet. Long flights and airport lounges have a way of compressing the news cycle - the Iran crisis, the Trump tariffs, the AI capex spree all flattening onto the same little seat-back screen with the same little chart and the same upward slope.

From altitude, the threats markets were supposed to be afraid of, look very small.

Notice what AI has just done. A year ago, investors had decided tariffs were the central risk to the US economy. This year, they had decided the Iran crisis was the central risk. Two weeks of strong performance later, both have been quietly forgotten. The same investors who, until very recently, were warning that AI was an energy guzzler in a country that didnt have enough power to spare - they are now back to celebrating the US AI trade as if energy weren’t an input at all. The US is, granted, a net exporter of energy. But the way the commentary has been going on - its as if oil prices (or gas) are just not an input into power generation or as if oil gas prices do not operate in a global world.

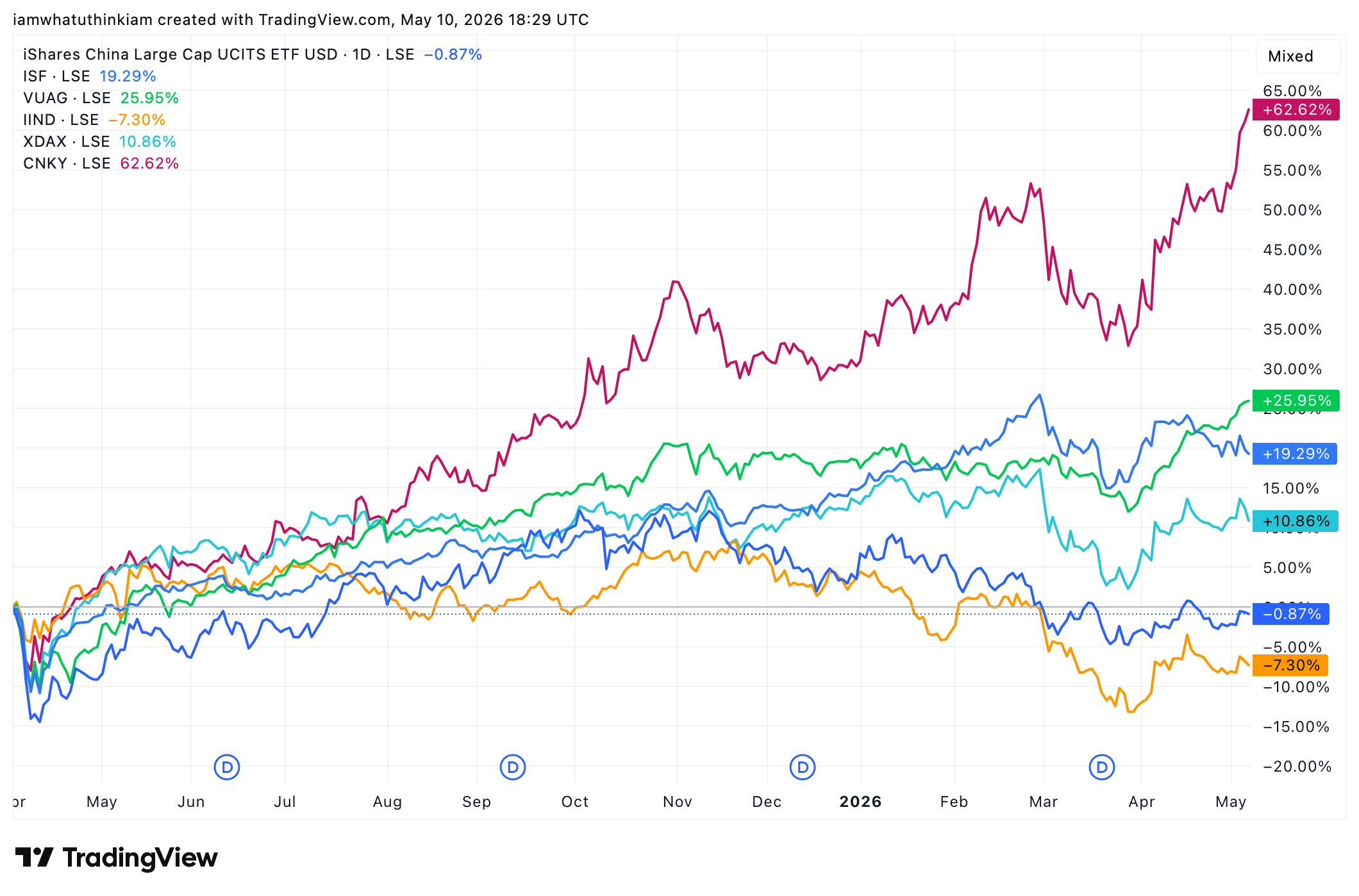

Here is what got my attention. The US stock market has, in two weeks, eliminated all the weak performance from the last several months. It is now back in pole position against the other major global markets (bar Japan). See below.

The chart shows the action since 1 April. After falling 10–15% in the aftermath of the tariff announcements, the US stock market is now up 26%. To make comparisons easier - so many currencies are involved - the chart is denominated in GBP via UK-listed ETFs. As you can see, neither the tariff war nor the Iran crisis could sink the market. The past two weeks have been pretty unkind to other markets that were doing quite well - like the UK - and the US has now pulled ahead significantly.

The old line still holds: if the US market catches a cold, everyone else gets a sneeze. So whether we like it or not, all of our portfolios are now hostage to one trade - the AI trade - continuing to play.

And the AI contribution to the US market is genuinely remarkable. A Wall Street Journal piece that landed in my reading list last week made the point in plain numbers (Link):

Personal consumption, the biggest component of GDP, grew a relatively muted 1.6%. Investment fell in … most other sectors … housing, business structures such as office buildings and factories, and transportation equipment like trucks and aircraft. Meanwhile, investment soared 43% in tech equipment, 23% in software and 22% in data-center buildings.

The article estimates that the AI economy grew 31%, the non-AI economy just 0.1%. The profit numbers tell the same story. Total S&P 500 earnings are on track to be up 27% in Q1, but the Mag-7 alone will be up 61%; the other 493 just 16% - a figure itself inflated by semiconductor companies like Micron.

Already, fund managers like Stephen Yiu of Blue Whale are speaking as if the hyperscalers themselves may or may not make money - but the picks-and-shovels plays will. The evidence isnt subtle. The Korean stock market, home to many memory makers, is up 78% this year. Taiwan now runs a trade surplus equal to 24% of its GDP. While I applaud the candour, it speaks poorly of what the investment world really thinks: not much of this AI capex is going to provide good returns to the people doing the spending.

This brings me to a thought I kept turning over at one of those airport lounges. Anthropic released 10 new agents relevant for Financial Services and me being me -wanted to give them a try. And in trying to install and run them I then I bumped into this video which brought some other thoughts to my mind.

Anthropic’s products are getting complex. To set up Cowork properly, you have to write a

.mdfile specifying preferences as basic as “dont delete files without my permission” - the kind of control any ERP gives you out of the box, because Sarbanes Oxley (SOx) and similar regulations elsewhere dont allow you to delete a row from a database without an audit trail.Is Anthropic on track to compete with SAP, Salesforce, Finacle as the next generation of business software? With one big difference - those companies run on an asset-light model; Anthropic carries a power-utility-sized compute capex base. Will start-up founders notice this and stop buying as much AI compute they have been buying off-late? After all who wants to pick up pennies in front of a road-roller?

One of the agents was month-end close! Thats a complex ERP functionality! Anyone who has lived through an ERP version change such as that of SAP ECC-to-S4HANA migration knows how difficult ERP design actually is. Customer workflows are sticky; New versions prove to be initially harder to use than the one they replace; teething issues take years to resolve. The market is currently pricing the AI trade as if “AI replaces software” is a clean substitution. The reality is closer to: AI vendors are now also software vendors — with all the design debt the job carries. With an existing corporate - why would one buy a brand new business software?

So what is likely to happen over the short to medium term? President Trump is still on track to meet Xi Jinping on 14–15 May. There is a reasonable chance hostilities with Iran dont break out again before that, providing a stable backdrop. Nvidia earnings land the week after - 20 May. Some of my readers may remember the accounting mechanics which mean that they can only be good.

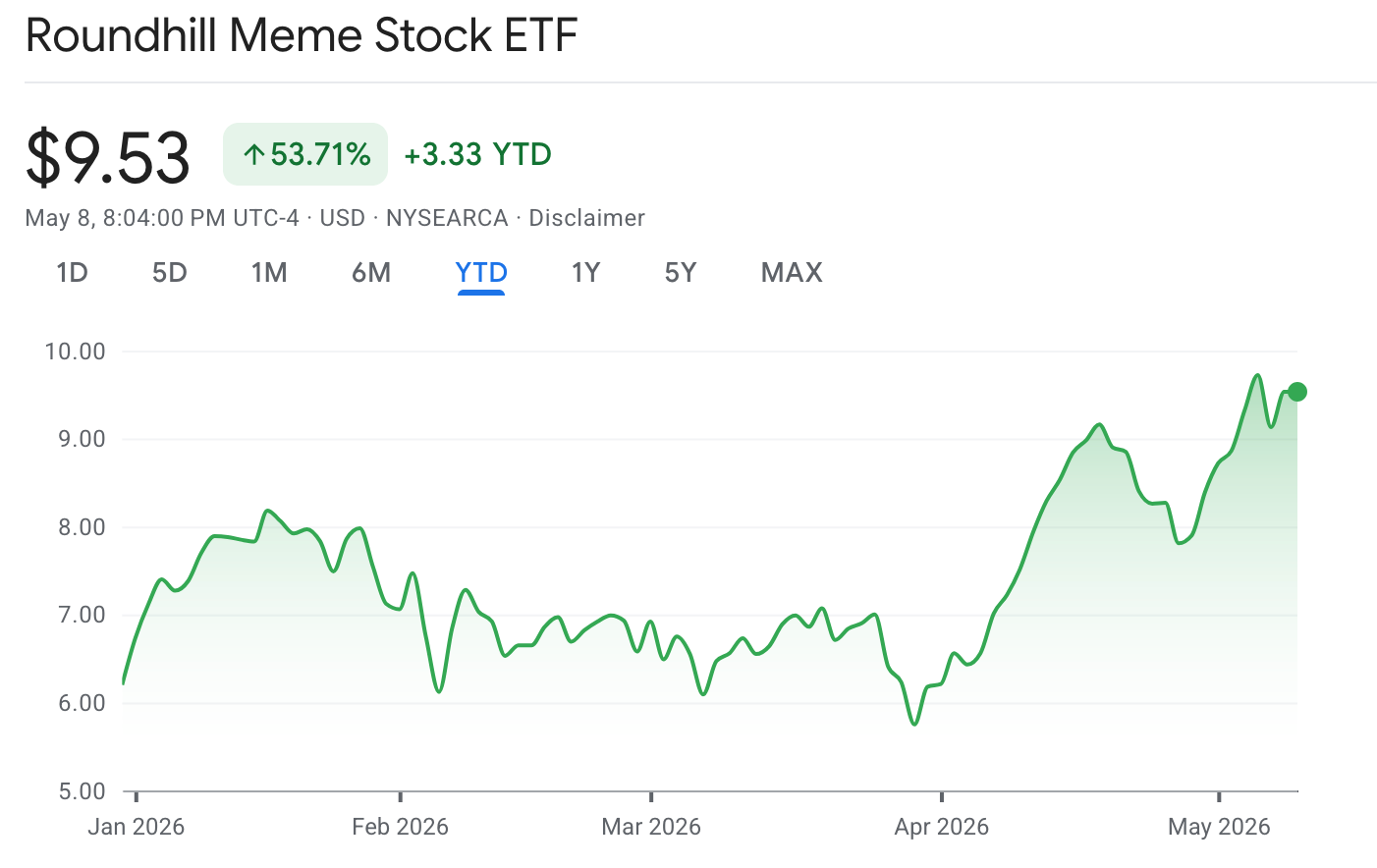

The dollar has been falling back to the lower part of its range, around 98, which is good for commodities. Gold and silver, after pulling back significantly from earlier highs, are quietly resuming their climb. The US equities volatility (VIX) continues its languorous slide and is now in one of the longest down-runs in a year. Bond volatility (MOVE) is being smothered by heavy, frequent Treasury buybacks of the off-the-run / weaker bonds Link, Link. The ETF of the snazziest stocks - the MEME ETF - is up 53% YTD.

At one level it looks like a party.

But here is what I have noticed. If something feels too good to be true, it often is. During the tariff-war stress of March 2025, it took 10-year Treasury yields at 4.6% to make the Trump administration pivot. During the Iran crisis, Treasuries reached 4.4% on Monday and Tuesday before the pivot happened. Watch that level.

Markets sometimes keep going up for a long time, and then fall quite rapidly - in just a few days. The 1999 model holds: dot-com investors enjoyed eighteen extra months of euphoria before the 2000 unwind, and most of them gave back more than they had made.

The other thing I have noticed is that if you stay long-term focused, the good times and the bad even out. Equity markets have an upward bias - companies can raise prices with inflation, which isnt true of any other asset class. So enjoy this long-in-the-tooth period of calm. Stay invested. Build the understanding to hold your nerve when the pivot finally arrives.

From 35,000 feet, the ground looks very far away. It is still there.

Just wanted to say that I look forward to your informative weekly post